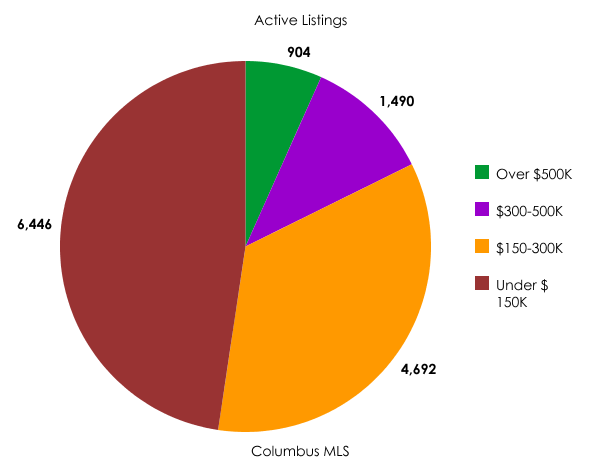

There were fewer homes listed for sale last month than is customary for September. Over the last five years, there was an average of 3,710 homes added to the market during the month of September. However, last month only 2,997 residential homes were added to the already elevated inventory in central Ohio.

Although slightly lower than August, the total residential listings in September (16,728) was still higher than it’s been since August of 2008 when the inventory level rose to 16,975.

“Inventory levels had come down over the last year and a half – which is what we were working towards,” said Sue Lusk-Gleich, President of the Columbus Board of REALTORS®. “When inventory levels are too high, the increased competition forces some homeowners to sell at prices that are too low which in turn often affects the values of other neighboring homes.”

“In order to re-balance the market, we either need the inventory to decrease or the number of buyers to increase. And since the tax credit incentives brought many buyers into the market earlier than we would have seen otherwise, we have a smaller pool of potential home buyers to absorb the inventory now.”

“When comparing sales figures to the previous year, we need to remember that home sales have been elevated since April of 2008 due to the tax credits,” adds Lusk-Gleich. “Even so, sales are still up four percent year to date.”

Home sales across Ohio were down 20.3 percent in September but are still up 1.5 percent for the first nine months of the year. The average sale price in Ohio last month was $129,572, down 3.5 percent from last September. Year to date (January through September), the average sale price was $134,318 which is down four percent compared to the first three quarters of 2009.

Nationwide, existing home sales - which are completed transactions that include single-family, townhomes, condominiums and co-ops- were down 19 percent. Distressed homes accounted for 35 percent of sales in September compared with 34 percent in August; they were 29 percent in September 2009.

The median sale price nationwide for all housing types in September was $171,700, down 2.4 percent from one year ago.

According to Freddie Mac, the national average commitment rate for a 30-year, conventional, fixed-rate mortgage fell to a record low 4.35 percent in September from 4.43 percent in August; the rate was 5.06 percent in September 2009.

Housing affordability is near an all-time record. Mortgage interest rates are almost half of what they were ten years ago and they’re about one-and-a-half points lower than the peak of the housing boom in 2005. At the same time, home prices are running about 22 percent less than five years ago when they were bid up by the biggest housing rush on record.

Click here for Ohio home sales statistics

Click here for the national home sales release

The Columbus Board of REALTORS® Multiple Listing Service (MLS) serves all of Franklin, Delaware, Fayette, Madison, Morrow, Pickaway and Union Counties and parts of Champagne, Clark, Hocking, Licking, Fairfield, Knox, Logan, Marion, and Ross Counties.